If you’ve gotten a Tax Certificate notice from your Wisconsin county or you know you owe back property taxes, this page is for you. I’m Mike Messmer, founder of Cash House Buyer WI. Over 30 years and more than 500 home purchases, I’ve handled a meaningful number of Wisconsin tax-delinquency situations — from owners one year behind who still had plenty of time, to owners with an active in-rem foreclosure petition where the 8-week redemption clock was running.

Wisconsin property tax delinquency is governed by Wis. Stat. Ch. 75, mainly Wis. Stat. § 75.521 — the in-rem foreclosure procedure used by Milwaukee County and most other Wisconsin counties. The timeline runs in three distinct stages, and most homeowners don’t understand which stage they’re in. This page lays the whole thing out plainly, shows you which decisions are still available at each stage, and explains where a cash sale fits — when it does, which isn’t every situation.

Heads up before we start: the timeline is slower than most people realize at the beginning, then much faster at the end. The county can’t begin foreclosure until your Tax Certificate has been outstanding for two full years. But once it files the in-rem petition in Circuit Court, the statutory redemption window is only 8 weeks. That window is the conversion moment. After it closes, the property goes to the county via tax deed and there’s no general statutory right of redemption from that point.

The Wisconsin Tax Delinquency Timeline — Three Stages

Stage 1 — The Tax Certificate (Year 1 of Delinquency)

If your property tax bill wasn’t paid by the deadline, your county treasurer issues a Tax Certificate on September 1 of the following year. The Tax Certificate is the formal start of the delinquency clock under Wis. Stat. § 75.521. The county sends written notice to all owners of record. Interest and penalties begin to accrue on the unpaid balance.

At this stage, you can pay the back taxes (plus accrued interest and penalties) directly to the county treasurer at any time and the Tax Certificate is satisfied. No court action has been filed. Nothing is on your title that affects sale or refinance other than the underlying tax lien itself.

Stage 2 — The 2-Year Threshold (Years 1-2)

This is the longest stage and the one where most homeowners do the least. Under Wis. Stat. § 75.521, the county cannot begin in-rem foreclosure until the Tax Certificate has been outstanding for TWO YEARS. That’s not ‘after two annual notices’ — it’s two years from the September 1 issuance of the Tax Certificate.

During this stage, two things are happening:

- Interest and penalties continue accruing on the original unpaid amount.

- If you don’t pay the second year’s taxes (because the first year is unaffordable too), a second Tax Certificate gets issued on the next September 1 — and now two separate years of delinquency are running on parallel tracks.

This stage is where the cash-sale option starts to make math-sense. You have time to plan a sale that pays off the back taxes at closing and preserves your remaining equity. The longer you wait, the more accumulated penalties and interest consume that equity.

Stage 3 — In-Rem Foreclosure (After 2 Years)

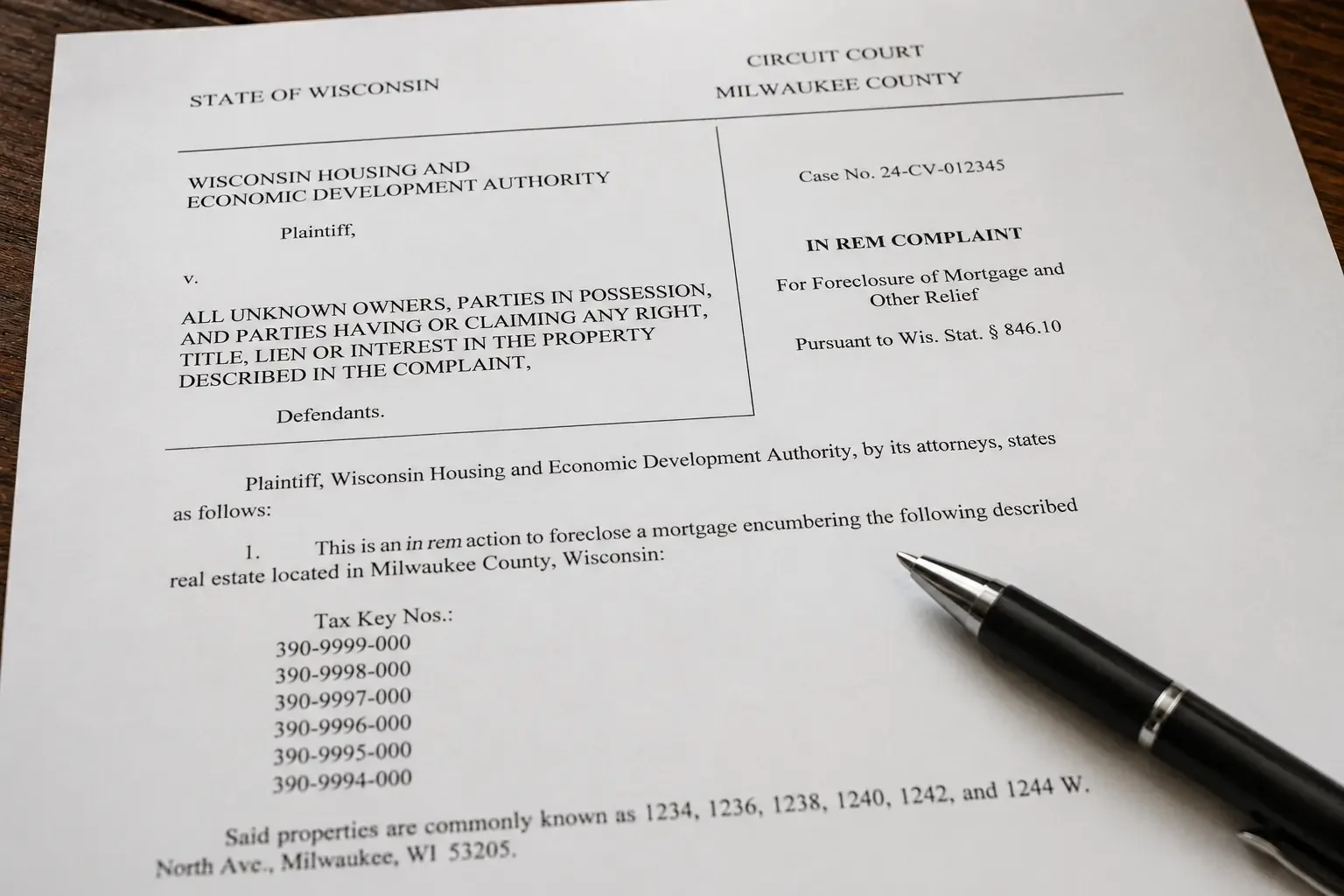

Once the Tax Certificate has been outstanding for 2 years, the county can file an in-rem foreclosure petition with the Circuit Court Clerk in your county. The county treasurer files: (1) a List of all properties being foreclosed, and (2) a Petition for Judgment of Foreclosure asking the court to transfer title to each parcel to the county. See Wis. Stat. § 75.521 for the full procedure.

Once the in-rem action is filed, several things happen on a defined statutory schedule:

If no objection is filed and no redemption occurs in the 8-week window, the Circuit Court enters a Judgment of Foreclosure transferring title to the county. The county then receives a tax deed. The former owner’s interest is extinguished.

Notice is sent to the last known address of all owners of record, all lenders, all other lienholders, and the municipality where the property is located.

Notice of the foreclosure action and the list of properties is published in a local newspaper for THREE CONSECUTIVE WEEKS.

A statutory redemption period of AT LEAST 8 WEEKS runs after the first publication. During this 8-week window, any owner or interested party may redeem the property by paying: (a) the unpaid taxes; (b) all accrued interest and penalties; (c) the reasonable costs the county incurred to initiate proceedings; and (d) the person’s share of the publication costs.

Under Wis. Stat. § 75.521(7), any person with an interest in or lien on the parcel can serve a verified Answer on the county treasurer objecting to the foreclosure on specific statutory grounds.

What Sellers Say About Cash House Buyer WI

“I hadn’t seen the house in 3 years. They still bought it.”

The property was falling apart and full of junk. Cash House Buyer WI gave me a fair offer and handled everything. I didn’t have to step inside once.

Jason Beezely

“The city was threatening to fine me. Cash House Buyer WI stepped in fast.”

I thought I was out of options. They gave me a cash offer in one day and closed before things got worse.

Pamela Newsom

The 8-Week Window — Why It’s the Critical Moment

Everything about Wisconsin tax delinquency comes down to the 8-week post-publication redemption window. Before publication, you have years to act calmly. During publication, you have weeks. After publication and the 8-week window, you have nothing — title transfers to the county, the tax deed is issued, and there is no general statutory right of redemption from the county at that point.

During the 8-week window, your real options are:

- Pay the redemption amount in full. The county releases the foreclosure. You keep the property.

- File a verified Answer under § 75.521(7) if you have a specific statutory ground to contest. Limited grounds — typically procedural defects in notice or jurisdiction, not ‘I disagree with the foreclosure.’ A Wisconsin attorney can advise on whether you have any.

- Sell the property. A traditional financed sale usually can’t close inside 8 weeks. A cash sale typically can — closing in 7 to 14 days, with the back taxes paid off from sale proceeds at closing and the rest of the equity coming to you.

- Do nothing and lose the property. After 8 weeks, the court enters judgment, title transfers to the county, and the former owner is extinguished.

City of Milwaukee — A Separate Track

If your property is in the City of Milwaukee (not just Milwaukee County), there’s a wrinkle: the City of Milwaukee operates its own in-rem tax foreclosure program separate from Milwaukee County’s process. Wisconsin first-class cities (Milwaukee is the only one) are authorized to pursue their own tax foreclosure procedures, and Milwaukee actively does so. Properties foreclosed by the city eventually show up in MLS listings flagged as ‘City of Milwaukee Tax Foreclosure Property.’ I cover this fully in Cluster 2, but if you’re inside city limits, that’s the program to look at — not the county’s.

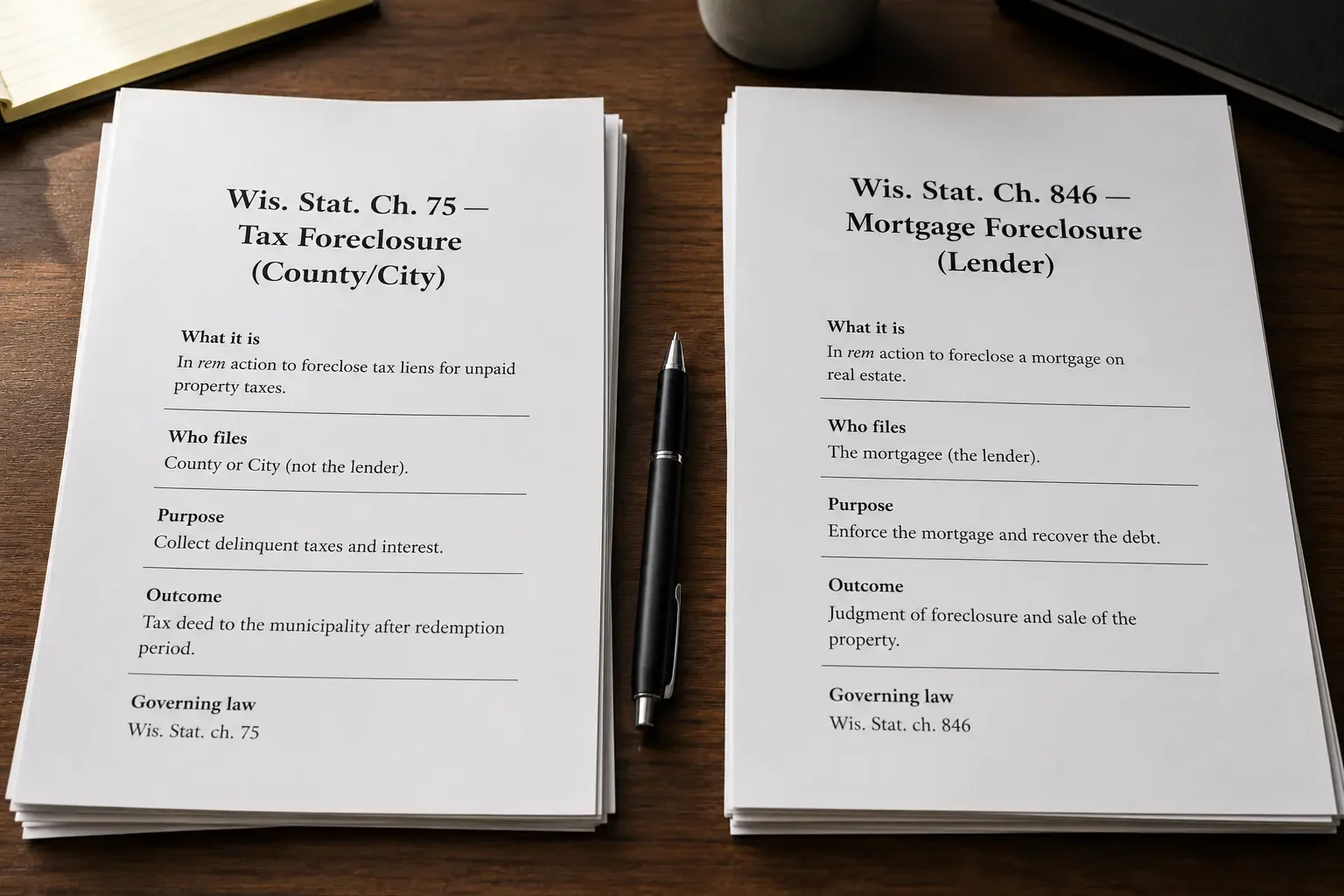

Tax Foreclosure vs Mortgage Foreclosure — Why They’re Different

Many Wisconsin homeowners with property tax problems also have mortgage problems. These are two completely separate procedures under two completely separate Wisconsin statute chapters. Property tax foreclosure runs under Wis. Stat. Ch. 75; mortgage foreclosure runs under Wis. Stat. Ch. 846. Different parties, different timelines, different procedures. I cover this fully in Cluster 3 — but the short version: if you have both problems, you have two different clocks running and the more urgent one isn’t always the more obvious one.

What a Cash Sale Looks Like in a Wisconsin Tax-Delinquency Situation

If you’re at any stage of the Wisconsin tax-delinquency timeline and a cash sale makes sense, here’s how it actually works with my team:

- Step 1: You call me. Direct line: (414) 246-0032. Or email Mike@cashhousebuyerwi.com. Tell me what county you’re in, how many years of back taxes are outstanding, and whether you’ve gotten any in-rem foreclosure notices. If you have notices, send me the document.

- Step 2: I walk the property. I see the actual condition, talk to you face-to-face, and confirm what I’m working with.

- Step 3: Written cash offer within 24 to 48 hours. The math accounts for the actual back-tax payoff (taxes + interest + penalties + any county costs) plus the actual condition of the home. I’m not pitching a national 70-percent-of-ARV formula — I’m pricing this specific situation.

- Step 4: If you accept, we coordinate with a Wisconsin title company. The title company confirms the exact redemption payoff with your county treasurer (or the City of Milwaukee for in-city properties), prepares closing documents, and handles the wire of redemption funds to the treasurer at closing.

- Step 5: Closing happens. Typically 7 to 14 days. The back taxes get paid off at closing from sale proceeds. The remaining equity comes to you. The in-rem foreclosure is satisfied.

Frequently Asked Questions

When does the Wisconsin property tax delinquency clock start?

It starts on September 1 of each year when the Wisconsin county treasurer issues a Tax Certificate for parcels with unpaid taxes, interest, penalties, special assessments, or special charges as of August 31 of that year. The Tax Certificate is the formal start of the delinquency procedure under Wis. Stat. Ch. 75.

How long before Wisconsin can foreclose for unpaid property taxes?

Two years from the date the Tax Certificate is issued. Under Wis. Stat. § 75.521, the county cannot file in-rem tax foreclosure until the Tax Certificate has been outstanding for two full years. The 2-year threshold is the most important date in Wisconsin tax delinquency planning.

How long is the redemption period after Wisconsin tax foreclosure is filed?

At least 8 weeks after the foreclosure action is first published in a local newspaper. During this redemption period, any owner or interested party can redeem by paying unpaid taxes, accrued interest and penalties, the county’s reasonable costs to initiate proceedings, and their share of publication costs under § 75.521(6).

Can I sell my Wisconsin home to a cash buyer if I owe back property taxes?

Yes. The closing pays off the full redemption amount to the county treasurer (or City of Milwaukee for in-city properties) from sale proceeds at closing. The in-rem foreclosure action is satisfied. Title transfers free and clear. Any remaining equity after the back-tax payoff and closing costs comes to the seller.

What happens after the Wisconsin in-rem tax foreclosure judgment is entered?

If no redemption occurs and no objection is sustained within the 8-week window, the Circuit Court enters a Judgment of Foreclosure transferring title to the county (or to the City of Milwaukee for in-city properties). The county or city receives a tax deed and the former owner’s interest is extinguished. There is no general statutory right of redemption from the county or city after the judgment.

Talk to Mike Directly

If you owe back property taxes in Wisconsin and you want a straight read on the math, give me a call. I’ll tell you which stage you’re in, what redemption would actually cost, and what a cash sale would look like — including the options that don’t involve selling to me. No pressure. Just the honest version. Call (414) 246-0032 or email Mike@cashhousebuyerwi.com. — Mike Messmer, Cash House Buyer WI.