Many Wisconsin homeowners with money trouble have both problems at the same time: they’re behind on their mortgage AND behind on their property taxes. These are two completely separate procedures governed by two completely separate Wisconsin statute chapters with different parties, different timelines, and different consequences. Most homeowners don’t know which one is more urgent.

This page lays them out side by side. I’m Mike Messmer — 30 years buying Wisconsin homes directly, and a meaningful percentage of those have been situations where both clocks were running. Here’s how to tell them apart and figure out which one to prioritize.

The Quick Comparison

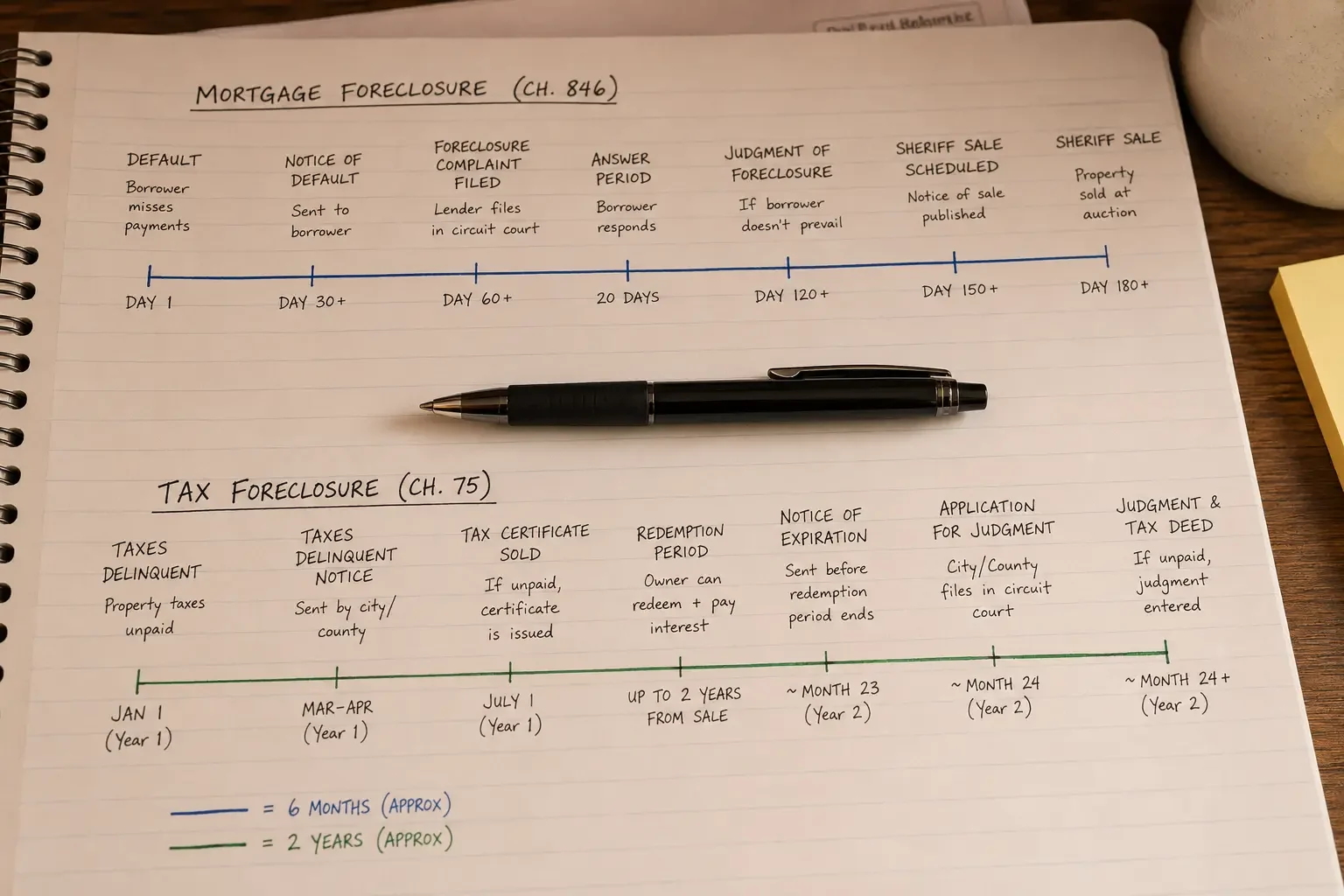

| Aspect | Mortgage Foreclosure (Wis. Stat. Ch. 846) | Tax Foreclosure (Wis. Stat. Ch. 75) |

| Who is foreclosing | Your mortgage lender or servicer | Your county treasurer (or City of Milwaukee for in-city) |

| Why | You missed mortgage payments | You missed property tax payments |

| Trigger | 120+ days delinquent on payments (federal CFPB rule) | Tax Certificate issued each Sept 1 for prior year delinquency |

| Threshold | Lender can file in court after 120 days delinquent | County can foreclose after 2 years from Tax Certificate |

| Typical total timeline | 8-14 months from court filing to sheriff sale | 2 years + 3-4 months after in-rem petition |

| Where filed | Circuit Court foreclosure action | Circuit Court in-rem petition |

| Notice required | Summons and Complaint personal service | Mail notice + 3 weeks newspaper publication |

| Statutory redemption | 12 mo (deficiency) or 6 mo (no deficiency) after judgment | At least 8 weeks after first publication |

| Sale procedure | Sheriff sale + court confirmation | Court enters judgment; tax deed issues to county |

| Post-event redemption | NO general post-sale redemption | NO general post-judgment redemption |

| Outcome on judgment | Title to highest bidder at sheriff sale (often the lender) | Title to county (or City of Milwaukee) |

| Reinstatement option | Yes — § 846.05 (dismisses if pre-judgment) | No equivalent — only full redemption |

What Sellers Say About Cash House Buyer WI

“I hadn’t seen the house in 3 years. They still bought it.”

The property was falling apart and full of junk. Cash House Buyer WI gave me a fair offer and handled everything. I didn’t have to step inside once.

Jason Beezely

“The city was threatening to fine me. Cash House Buyer WI stepped in fast.”

I thought I was out of options. They gave me a cash offer in one day and closed before things got worse.

Pamela Newsom

The Same Statutory Structure

Although the city’s program is operationally distinct, the underlying statute is the same. The in-rem foreclosure procedure under Wis. Stat. § 75.521 applies to both county and city programs. That means:

- The 2-year delinquency threshold applies before foreclosure can begin.

- The city files a List of properties and a Petition for Judgment of Foreclosure with the Circuit Court Clerk.

- Notice goes to owners, lenders, lienholders, and the municipality.

- Publication for 3 consecutive weeks in a local newspaper.

- Statutory redemption period of at least 8 weeks after first publication.

- Redemption amount: unpaid taxes + interest + penalties + reasonable city costs + share of publication costs under § 75.521(6).

- Right to Answer under § 75.521(7) — limited statutory grounds, served on the city treasurer.

- If no redemption and no successful objection, judgment transferring title to the city.

If You Have Both Problems

Many Wisconsin homeowners with one of these problems have both. The cause is usually the same — household income or savings can’t keep up with both the monthly mortgage and the lump-sum property tax bills. The implication is that you have TWO separate procedural clocks running, neither of which automatically slows down because of the other.

- Which one is more urgent depends on where you are in each timeline:

- Mortgage default with property taxes current. The mortgage problem is your priority. Wis. Stat. Ch. 846 mortgage foreclosure timeline is faster than tax delinquency timeline in most situations.

- Property tax delinquency with mortgage current. The tax problem is technically less urgent in years 1-2 (no procedural action yet) but becomes very urgent at year 2+ when the in-rem petition can be filed.

- Both problems with both clocks well advanced. Whichever procedure is closer to its decisive moment (mortgage sheriff sale vs tax deed) is the more urgent. A cash sale can resolve BOTH simultaneously — the closing pays off both the mortgage and the back taxes from sale proceeds, and the rest of the equity (if any) comes to you.

Why a Cash Sale Solves Both

If you’re caught between mortgage foreclosure and tax foreclosure with both clocks running, a cash sale resolves both simultaneously. Here’s the mechanics:

- The Wisconsin title company prepares a closing statement that includes BOTH the mortgage payoff (from the lender) and the tax redemption amount (from the county treasurer or City of Milwaukee).

- At closing, the buyer’s funds wire to the title company.

- The title company disburses: mortgage payoff to the lender (releases the mortgage and stops the foreclosure under Ch. 846); tax redemption payoff to the county/city treasurer (satisfies the in-rem proceeding under Ch. 75); closing costs; and any remaining equity to you.

- Title transfers to the cash buyer free and clear of both encumbrances. Both procedures end. You’re out from under both clocks.

This is one of the cleanest applications of a cash sale to a Wisconsin distressed-property situation. You’re not playing one statute against the other or trying to extend one clock while the other runs out. You’re closing both at the same time on the same day.

Read the Companion Posts

If you want the deeper version of either side: Wisconsin Foreclosure & Sheriff Sale — Wis. Stat. Ch. 846 (Campaign 1) covers the mortgage side in full. The Pillar and Cluster 1/Cluster 2 of this campaign cover the tax side.

Talk to Mike

If you have both a mortgage problem and a tax problem and you want to talk through the math, call me at (414) 246-0032 or email Mike@cashhousebuyerwi.com. I’ll give you a straight read on which clock is more urgent and what a cash sale would look like for your specific combination. — Mike.

Frequently Asked Questions

What’s the difference between Wisconsin tax foreclosure and mortgage foreclosure?

Tax foreclosure is initiated by your county treasurer (or City of Milwaukee for in-city properties) under Wis. Stat. Ch. 75 when property taxes are unpaid. Mortgage foreclosure is initiated by your lender under Wis. Stat. Ch. 846 when mortgage payments are unpaid. Different statutes, different parties, different timelines, different procedures. Both end with you losing the property if no action is taken.

Which Wisconsin foreclosure is faster — tax or mortgage?

Mortgage foreclosure is typically faster once initiated (8-14 months from filing to sheriff sale, with a 6 or 12 month statutory redemption period under § 846.10). Tax foreclosure has a longer lead-in (2 years from Tax Certificate before in-rem petition can be filed) but a much shorter window once filed (8-week redemption period after first publication under § 75.521).

What if I have both mortgage and tax delinquency on the same Wisconsin property?

You have two separate clocks running, governed by two separate statutes. Neither slows down because of the other. Determining which is more urgent depends on where you are in each timeline. A cash sale can resolve both simultaneously — the closing pays off the mortgage AND the back taxes from sale proceeds, satisfying both procedures at one closing.

Can a single cash sale resolve both Wisconsin tax foreclosure and mortgage foreclosure?

Yes. The title company prepares a closing statement that includes the mortgage payoff (to the lender) and the tax redemption amount (to the county or City of Milwaukee). At closing, both are wired to the respective parties. The mortgage is released (satisfying Ch. 846), the tax redemption is completed (satisfying Ch. 75), and title transfers free and clear of both encumbrances.