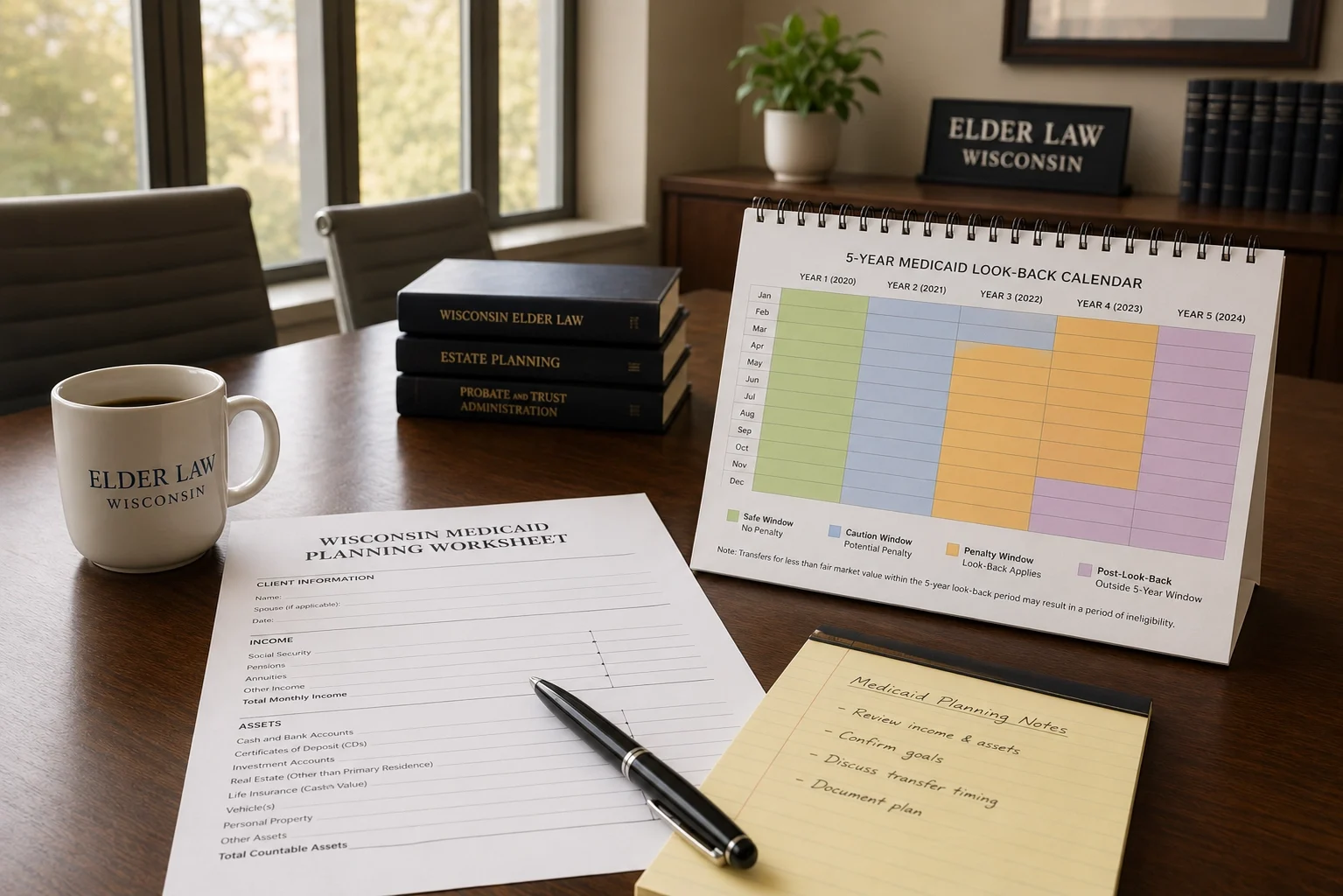

If your Wisconsin family is thinking about Wisconsin Medicaid Long-Term Care — nursing home Medicaid, Wisconsin Family Care, or Family Care Partnership — within the next five years, the federal Medicaid 5-year lookback matters. The lookback reviews asset transfers in the preceding 60 months when evaluating Medicaid eligibility. Transfers below fair market value during that window can create penalty periods of ineligibility.

The 5-year lookback is one of the most widely misunderstood elements of senior financial planning. Most families either ignore it entirely (which can create costly surprises) or panic about it inappropriately (which leads them to avoid healthy planning steps that wouldn’t actually create lookback problems). This page lays out what the lookback actually does, how it interacts with a Wisconsin home sale, and where the cash-sale option fits in the planning math. I’m Mike Messmer; 30 years buying Wisconsin homes directly. Here’s the practical version — but consult a Wisconsin elder law attorney before any major decisions because the planning is genuinely complex.

What the 5-Year Lookback Actually Is

When a Wisconsin senior applies for Wisconsin Medicaid Long-Term Care (Nursing Home Medicaid, HCBS Waivers via Family Care or Family Care Partnership, or EBD Medicaid), Wisconsin’s Department of Health Services reviews the applicant’s asset transfers during the preceding 60 months. This 5-year period is the federal Medicaid lookback, established under federal Medicaid law and applied uniformly across all states.

The review looks at one specific category of transfers: assets given away, transferred for less than fair market value, or otherwise disposed of without adequate consideration in return. Specifically:

- Gifts to children, grandchildren, friends, or family members.

- Charitable donations made during the lookback period.

- Transfers to certain types of irrevocable trusts.

- Sales of property below fair market value (e.g., selling the home to a family member at a discount).

- Other dispositions where the senior received less than full value in return.

What the lookback DOES NOT typically capture:

- Regular living expenses (rent, food, utilities, medical care).

- Fair-market-value sales (e.g., selling the home to a buyer at fair market value — the senior received full value, so no transfer penalty).

- Spending on the senior’s own care (private-pay assisted living, memory care, nursing home, in-home care).

- Spending on certain Medicaid-allowed planning uses (some pre-paid funeral expenses, certain home modifications for a spouse, payment of debts).

What Sellers Say About Cash House Buyer WI

“I hadn’t seen the house in 3 years. They still bought it.”

The property was falling apart and full of junk. Cash House Buyer WI gave me a fair offer and handled everything. I didn’t have to step inside once.

Jason Beezely

“The city was threatening to fine me. Cash House Buyer WI stepped in fast.”

I thought I was out of options. They gave me a cash offer in one day and closed before things got worse.

Pamela Newsom

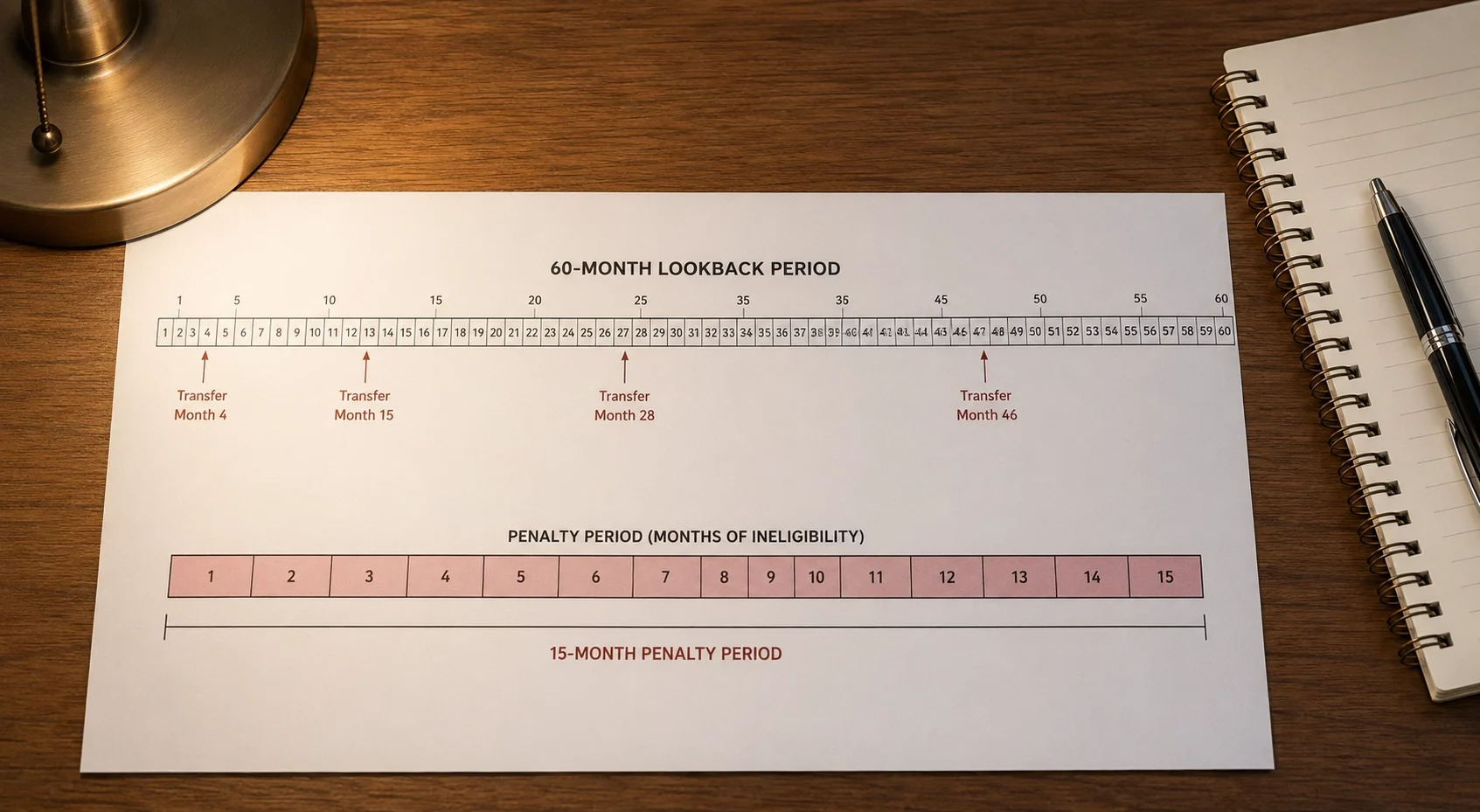

The Penalty Period — How It Works

If the lookback identifies a transfer that violates the rules, the consequence is a penalty period of Medicaid ineligibility. The penalty period length is calculated by dividing the value of the transferred asset by Wisconsin’s monthly nursing home private-pay rate (currently roughly $9,855, though the state uses a specific divisor that may differ slightly from the published market rate).

Example: A Wisconsin senior gifts $50,000 to her daughter in year 3 of the lookback window. Two years later, she enters a nursing home and applies for Medicaid. The $50,000 gift creates a penalty period of approximately 50,000 ÷ 9,855 = ~5 months of Medicaid ineligibility. During those 5 months, the senior must private-pay for her nursing home care even though her assets and income otherwise qualify for Medicaid.

The penalty period starts when the senior would otherwise be Medicaid-eligible — meaning it starts after assets have been spent down to the eligibility limit. This timing makes the penalty meaningfully more painful than people often realize, because the senior is already at the point of needing Medicaid before the penalty even begins to run.

How a Wisconsin Home Sale Interacts with the Lookback

This is where it gets nuanced. Selling the Wisconsin family home AT FAIR MARKET VALUE does not create a lookback problem by itself. The senior received full value (the sale proceeds) in exchange for the asset (the home). No transfer penalty. This is true whether the sale is to a financed buyer, to a cash buyer like Cash House Buyer WI, or to anyone else paying fair market value.

The lookback issues arise from what happens AFTER the sale. Specifically:

- If sale proceeds are gifted to children or other family members during the lookback window, those gifts can trigger penalties.

- If sale proceeds are donated to charity during the lookback window, the donations can trigger penalties.

- If sale proceeds are transferred to certain irrevocable trusts during the lookback window, the transfers can trigger penalties.

- If sale proceeds are used to buy assets that are then transferred at less than fair value, those transactions can be scrutinized.

The home itself, while occupied by the senior or a spouse, is initially exempt from the Medicaid asset count. So in a household where the senior is still living in the home, the home doesn’t yet count toward the $2,000 asset limit. But once the senior moves permanently to a nursing home, the home typically becomes a countable asset (subject to a federal home equity limit). Selling the home converts an initially-exempt asset (while occupied) or an actually-countable asset (post-institutionalization) into liquid cash that does count.

Wisconsin Medicaid Estate Recovery

Wisconsin pursues Medicaid Estate Recovery after a Medicaid Long-Term Care recipient passes away. Wisconsin Department of Health Services can recover Medicaid expenditures from the recipient’s estate — including any home equity that returns to the estate.

This is the consideration that motivates many Wisconsin families to sell the family home earlier in the process and structure the proceeds to fund care directly rather than allowing the home equity to flow into the estate where it becomes subject to recovery. The Wisconsin Long-Term Care Partnership Program provides asset protection (and estate recovery protection) for benefits paid by qualifying LTC insurance policies — but most current Wisconsin seniors don’t have a Partnership-qualifying policy.

Practical Planning Implications

For Wisconsin families weighing a home sale with potential Medicaid timing implications:

- Selling the home at fair market value is fine. The sale itself doesn’t create lookback problems. Cash House Buyer WI’s offers are at fair market value for as-is condition — the sale documentation reflects this.

- Using sale proceeds to fund the senior’s own care is fine. Private-pay assisted living, memory care, nursing home — all legitimate uses with no lookback problem.

- Gifts and transfers within the 5-year window require planning. If proceeds are going to be given to children, donated, or transferred to a trust, the timing and structure matter. A Wisconsin elder law attorney can structure these in ways that minimize lookback impact.

- The 5-year clock is real. Planning that spans 5+ years before Medicaid application is needed has more flexibility than planning done in the year or two before application.

- Consult a Wisconsin elder law attorney before major decisions. The State Bar of Wisconsin’s Lawyer Referral and Information Service can connect families with experienced attorneys. The cost of consultation is far less than the cost of a Medicaid penalty period.

Wisconsin Has NO State Estate Tax / NO State Inheritance Tax

Worth restating here because it matters for the Medicaid planning math: Wisconsin has no state estate tax and no state inheritance tax. When a Wisconsin senior eventually passes, whatever assets remain in the estate pass to heirs without state-level tax friction. This is meaningfully different from states like Pennsylvania (4.5% inheritance tax on lineal descendants), Iowa, or Nebraska.

Combined with Wisconsin Medicaid Estate Recovery (which DOES pursue estate assets to recover Medicaid expenditures), the planning math is: assets used during life for the senior’s own care are gone forever; assets that survive in the estate at death first satisfy any Medicaid recovery claim, then pass to heirs without state tax. Federal estate tax only applies to estates over ~$13.9M, which doesn’t apply to typical Wisconsin senior families.

Frequently Asked Questions

Does selling a Wisconsin home at fair market value trigger the Medicaid 5-year lookback?

No. Selling at fair market value does not create a lookback problem by itself — the senior receives full value in exchange for the asset. The lookback issues arise from what happens AFTER the sale, particularly gifts of sale proceeds to children, charitable donations, or transfers to certain trusts within the 5-year window.

What is the Wisconsin Medicaid 5-year lookback?

When a Wisconsin senior applies for Wisconsin Medicaid Long-Term Care (Nursing Home Medicaid, HCBS Waivers via Family Care or Family Care Partnership, or EBD Medicaid), Wisconsin Department of Health Services reviews asset transfers in the preceding 60 months. Transfers below fair market value during this window can create penalty periods of ineligibility, calculated by dividing the transferred amount by Wisconsin’s monthly nursing home rate divisor.

Is the home counted as an asset for Wisconsin Medicaid?

The home is initially exempt while the senior (or a spouse) lives there, subject to a federal home equity limit. Once the senior moves permanently to a nursing home, the home typically becomes a countable asset. Selling the home converts an initially-exempt (while occupied) or actually-countable (post-institutionalization) asset into liquid cash that does count toward the asset limit.

Does Wisconsin pursue Medicaid Estate Recovery?

Yes. Wisconsin pursues Medicaid Estate Recovery after a Medicaid Long-Term Care recipient passes — recovering Medicaid expenditures from the recipient’s estate, including any home equity that returns to the estate. The Wisconsin Long-Term Care Partnership Program provides asset protection (and estate recovery protection) for benefits paid by qualifying LTC insurance policies.

How Cash House Buyer WI Fits in Wisconsin Medicaid Planning

Cash House Buyer WI is one of the tools available to Wisconsin families navigating senior Medicaid planning. The role is specific: I buy homes at fair market value for as-is condition. The sale proceeds go to the senior or to a structure the family’s elder law attorney has set up. The procedural cleanliness of the closing — Wisconsin title company handling everything, no inspection contingencies, 7-14 day timeline — is the operational value.

I’m not an attorney. I don’t structure Medicaid trusts, prepare gift letters, or advise on lookback timing. Wisconsin elder law attorneys do that work, and I refer families to qualified ones when needed. What I do is convert the Wisconsin family home into liquid funds quickly and at fair value, with the procedural moving parts handled cleanly. The family and their attorney decide what to do with the proceeds; my role is just the sale.

Call me at (414) 246-0032 or email Mike@cashhousebuyerwi.com to talk through whether a cash sale fits your family’s Medicaid planning timeline. — Mike.