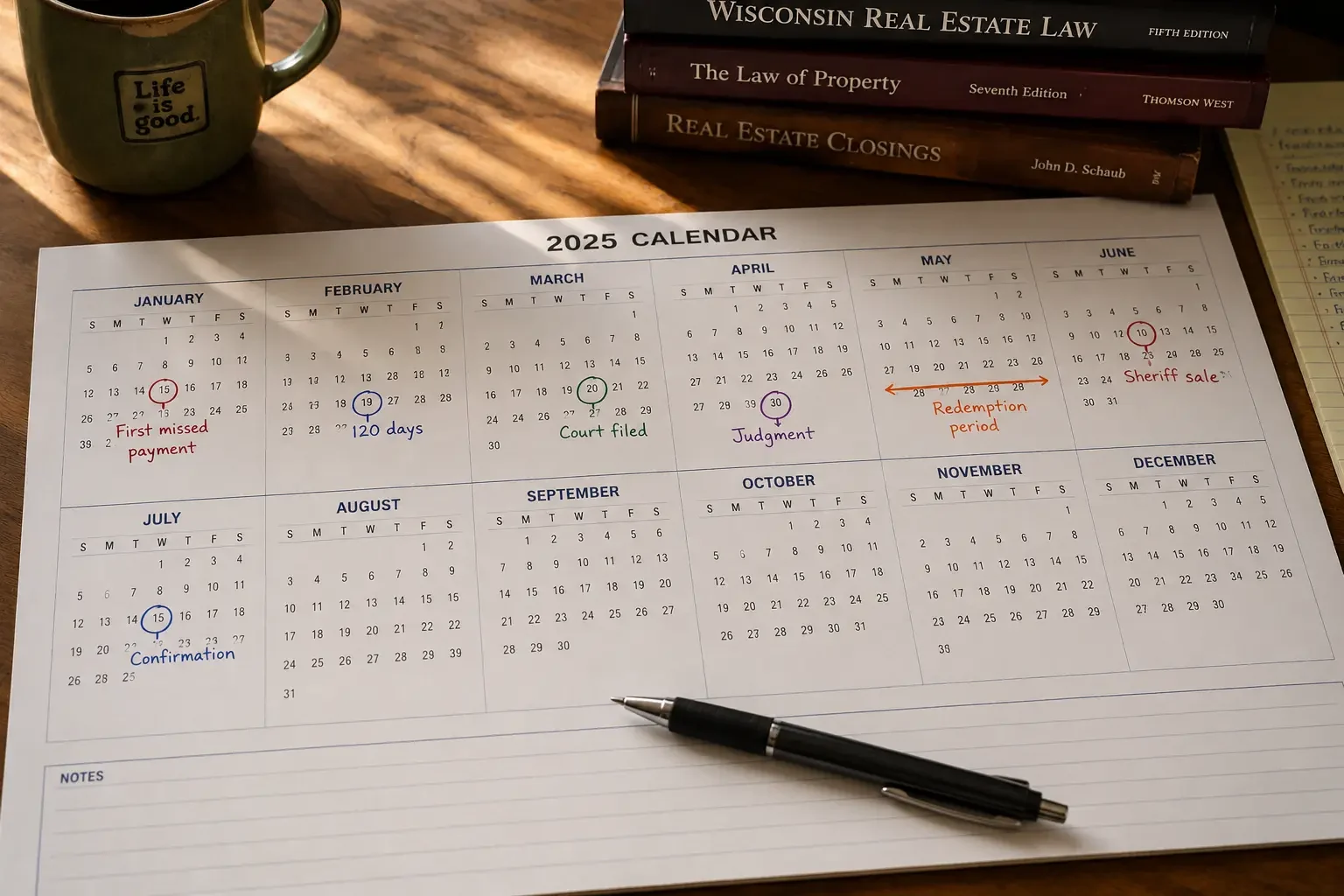

One of the first questions Wisconsin homeowners ask when they fall behind on a mortgage is: how long do I actually have? It’s the right question. The Wisconsin foreclosure process is structured in stages, and the time you have to act depends entirely on which stage you’re in.

This page walks through the full timeline — from your first missed payment all the way to the sheriff sale and court confirmation — with the specific statutory anchors that govern each stage. I’m Mike Messmer; I’ve watched this timeline play out more than 500 times in 30 years of buying Wisconsin homes directly. Here’s the honest version.

Months 1-4: The Federal 120-Day Pre-Filing Window

Your first missed payment doesn’t put you in foreclosure. Under federal CFPB rules, mortgage servicers generally cannot make the first foreclosure filing until you’re more than 120 days delinquent. That’s a four-month window in which the lender will be contacting you — by mail, by phone, sometimes by visit — to discuss loss mitigation.

During this window, your options are widest:

- Bring the loan current and stop the process entirely.

- Request a loan modification, forbearance, or repayment plan.

- Talk to a free HUD-approved housing counselor (hud.gov/findacounselor) about your options.

- List the home traditionally and sell on the open market.

- Sell for cash to a buyer who specializes in pre-foreclosure situations.

Most homeowners in this window are still in denial or in shock. They’re not opening the lender’s mail and not returning phone calls. I understand — but every week that passes in this window is a week of options you’re letting expire. The earlier you act, the more equity you preserve.

What Sellers Say About Cash House Buyer WI

“I hadn’t seen the house in 3 years. They still bought it.”

The property was falling apart and full of junk. Cash House Buyer WI gave me a fair offer and handled everything. I didn’t have to step inside once.

Jason Beezely

“The city was threatening to fine me. Cash House Buyer WI stepped in fast.”

I thought I was out of options. They gave me a cash offer in one day and closed before things got worse.

Pamela Newsom

Month 4-5: The Foreclosure Filing

After more than 120 days delinquent, the lender’s attorney files a Summons and Complaint in the Wisconsin Circuit Court of the county where your property is located. The action is governed by Wis. Stat. Ch. 846. You’ll be served either personally by the sheriff or by a process server.

Once served, you have a limited window to file an Answer with the court — usually 20 days for personal service, 45 days for service by publication if the lender can’t find you. Not filing an Answer means the lender can request a default judgment, which is the fastest path to sheriff sale.

This is also the stage where you should be talking to a Wisconsin foreclosure attorney. Some defenses — improper notice, defective assignment of the mortgage, predatory lending — only exist before judgment. The State Bar of Wisconsin’s Lawyer Referral and Information Service can connect you with one.

Month 5-7: Judgment of Foreclosure

Either by default (no Answer filed) or after motion practice, the court eventually enters a Judgment of Foreclosure. This is the procedural milestone that starts the redemption clock. The judgment will state:

- The full amount owed to the lender including principal, interest, late fees, attorney fees, and costs.

- Whether the lender is preserving the right to seek a deficiency judgment or has waived it (this determines whether your redemption period is 12 months or 6 months).

- The procedure for the future sheriff sale.

Under Wis. Stat. § 846.05, reinstatement BEFORE judgment results in dismissal of the foreclosure action. Reinstatement AFTER judgment but before sale stays the foreclosure but doesn’t dismiss it — if you default again, the foreclosure proceeds.

Months 7-18: The Redemption Period

This is the longest stretch of the Wisconsin foreclosure timeline. Under Wis. Stat. § 846.10, for owner-occupied 1-4 family residential property:

- 12 months from the date of judgment if the lender retains the right to seek a deficiency judgment.

- 6 months from the date of judgment if the lender waives the right to a deficiency judgment.

This is also the longest practical window to sell the home and stop the foreclosure entirely. During the redemption period, the sheriff sale CANNOT happen. The lender has to wait. If you can sell during this window, the sale proceeds pay off the judgment at closing and any remaining equity comes to you.

Two shortened-redemption variations exist for specific situations:

- Wis. Stat. § 846.101 — 5-week redemption period for abandoned property. Requires the lender to make a specific election in the complaint and prove abandonment under statutory criteria.

- Wis. Stat. § 846.102 — 2-month redemption period for certain owner-occupied/abandoned situations.

Month 12-18: The Sheriff Sale

After the redemption period expires, the lender schedules a sheriff sale. Notice of sale is published in a local newspaper for several weeks before the date. The sheriff (or, in some cases, a court-appointed referee) conducts a public auction — usually at the courthouse, usually within a few minutes per property.

At the sale itself, the lender typically bids the full judgment amount (called a ‘credit bid’). Outside investors can bid higher in cash. Whoever wins receives a Sheriff’s Certificate of Sale, but title doesn’t actually transfer until the court confirms the sale.

Final Step: Court Confirmation

The sheriff files a report of sale with the court. The court reviews and either confirms the sale or, very rarely, sets it aside. Confirmation is the procedural step that finalizes the foreclosure. Once confirmed:

- Title transfers to the purchaser (usually the lender, sometimes an outside investor).

- There is no general statutory right of redemption in Wisconsin after confirmation.

- If the former homeowner is still in the property, the purchaser can request a writ of assistance directing the sheriff to remove them.

Frequently Asked Questions

When does the Wisconsin foreclosure clock actually start?

Two clocks run. The federal CFPB 120-day rule prevents most mortgage servicers from filing foreclosure until you’re more than 120 days delinquent — so your first missed payment starts the pre-filing clock. The lender then files in Wisconsin Circuit Court, and the judicial timeline begins. The statutory redemption clock under Wis. Stat. § 846.10 doesn’t start until the court enters Judgment of Foreclosure.

What is the federal 120-day foreclosure rule?

Under Consumer Financial Protection Bureau (CFPB) regulations, mortgage servicers generally cannot make the first foreclosure filing on most owner-occupied loans until the borrower is more than 120 days delinquent. This gives most homeowners a four-month window during which the lender will be contacting them for loss mitigation discussions but cannot file in court.

What happens between judgment and sheriff sale in Wisconsin?

The statutory redemption period runs. Under Wis. Stat. § 846.10, the period is 12 months from judgment if the lender retains the right to seek a deficiency judgment, or 6 months if the lender waives the deficiency. During this period, the sheriff sale cannot occur. The homeowner can reinstate (under § 846.05), redeem in full, or sell the property to end the foreclosure.

Can the Wisconsin redemption period be shortened?

Yes, in two situations. Wis. Stat. § 846.101 provides a 5-week redemption period for abandoned property. Wis. Stat. § 846.102 provides a 2-month redemption period for certain owner-occupied/abandoned situations. Both require the lender to make a specific election in the foreclosure complaint and prove the property meets statutory criteria.

Where a Cash Sale Fits on This Timeline

The honest answer is: anywhere before court confirmation, but earlier is almost always better. The most common cash-sale windows are pre-filing (months 1-4) and the redemption period (months 7-18 of a typical full timeline). At every stage before sheriff sale confirmation, the cash sale resolves the foreclosure by paying off the judgment at closing and getting you the remaining equity. After confirmation, there’s no path back.

Call me at (414) 246-0032 or email Mike@cashhousebuyerwi.com. I’ll give you a straight read on which window you’re in and what the math actually looks like. — Mike.