Two of the most important — and most confused — concepts in Wisconsin foreclosure are reinstatement and redemption. They sound similar. They’re different. Wisconsin homeowners who confuse them often lose options that were available to them. This page explains both, where they apply on the timeline, and what each one actually costs.

I’m Mike Messmer. 30 years of buying Wisconsin homes directly, more than 500 acquisitions, a lot of them inside one or both of these windows. Here’s how each one works in plain language.

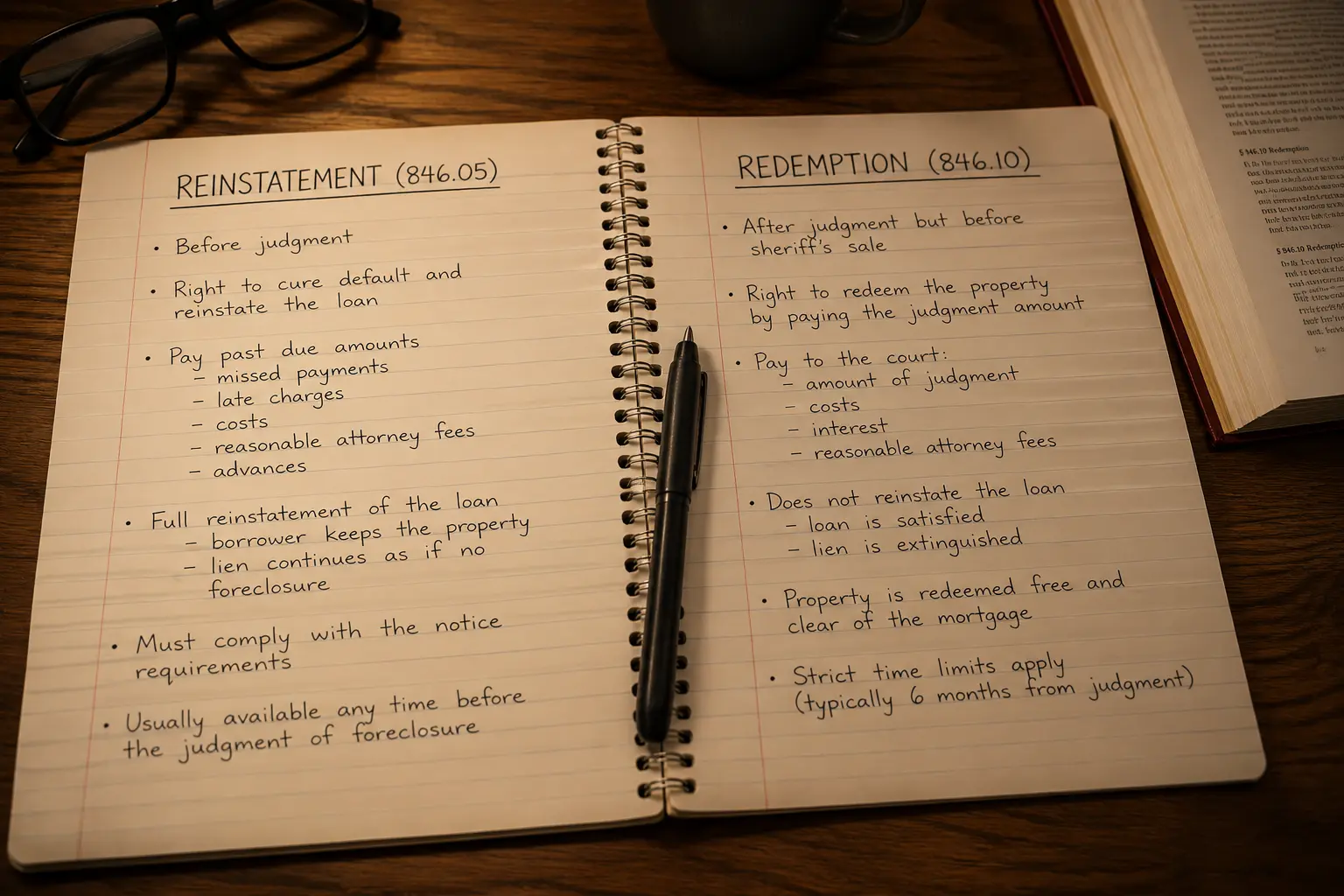

Reinstatement — Wis. Stat. § 846.05

Wis. Stat. § 846.05 gives a Wisconsin foreclosure borrower the right to reinstate the mortgage loan by paying everything that’s currently past due — missed payments, late fees, interest, attorney fees, and court costs. Reinstatement brings the loan back to current. Future payments resume on the original schedule.

The key fact most homeowners miss: reinstatement works differently depending on when you do it.

- Reinstatement BEFORE judgment: the court dismisses the foreclosure action entirely. The foreclosure is gone. If you default again later, the lender has to start the whole process over from scratch.

- Reinstatement AFTER judgment but BEFORE sale: the foreclosure is stayed (paused). The judgment remains on file. If you default again, the foreclosure proceeds from where it was — the lender doesn’t have to refile.

This is a real distinction. Pre-judgment reinstatement gives you a fresh start. Post-judgment reinstatement is more like a probationary pause — the lender keeps the leverage of an existing judgment if you stumble again. If you have the cash to reinstate, doing it before judgment is almost always better.

What Sellers Say About Cash House Buyer WI

“I hadn’t seen the house in 3 years. They still bought it.”

The property was falling apart and full of junk. Cash House Buyer WI gave me a fair offer and handled everything. I didn’t have to step inside once.

Jason Beezely

“The city was threatening to fine me. Cash House Buyer WI stepped in fast.”

I thought I was out of options. They gave me a cash offer in one day and closed before things got worse.

Pamela Newsom

Redemption — Wis. Stat. § 846.10

Redemption is fundamentally different from reinstatement. Where reinstatement brings the loan current (pay what’s past due, keep the loan going), redemption pays off the entire judgment — typically the full loan balance plus all costs. After redemption, the loan is gone, and so is the foreclosure. The homeowner owns the property free and clear of that lender.

Under Wis. Stat. § 846.10, for owner-occupied 1-4 family residential property, the redemption period is:

- 12 months from the date of judgment if the lender keeps the right to a deficiency judgment.

- 6 months from the date of judgment if the lender waives the right to a deficiency.

The lender’s election (deficiency vs no deficiency) appears in the foreclosure complaint and the judgment. Why does the lender care? A deficiency judgment lets the lender pursue the homeowner personally for any shortfall between the sale price and the loan balance — but only after waiting longer. Lenders waive deficiency rights when they don’t expect a shortfall (when the home is worth more than the loan) or when pursuing the homeowner personally isn’t worth it.

During the redemption period:

- The homeowner generally remains in possession of the property until the sale.

- The sheriff sale cannot occur.

- The homeowner can pay off the full judgment at any time and end the foreclosure.

- The homeowner can sell the property — the closing pays off the judgment from sale proceeds and the rest of the equity goes to the homeowner.

Shortened Redemption Periods

Wisconsin has two shortened-redemption variations for specific situations. Wis. Stat. § 846.101 provides a 5-week redemption period for abandoned property. Wis. Stat. § 846.102 provides a 2-month redemption period for certain owner-occupied/abandoned situations. Both require the lender to make a specific election in the foreclosure complaint and prove the property meets the statutory criteria.

If your property is occupied and you’re paying utilities, mowing the grass, and using the home as a residence, these shortened periods generally don’t apply. But if you’ve moved out and the property has been sitting vacant, the lender may try to invoke § 846.101 or § 846.102 to speed up the timeline. Don’t assume you have 12 months until you’ve confirmed how the foreclosure complaint reads.

The Practical Decision Tree

Here’s how to think about which option applies to you:

- If you can bring the loan current and want to keep the home: REINSTATEMENT. Do it before judgment if at all possible (dismisses the action) rather than after judgment (just pauses it).

- If you can pay off the loan in full and want to keep the home: REDEMPTION. This happens during the 12-month or 6-month window after judgment.

- If you can’t bring the loan current AND you can’t pay it off but you have equity: SELL during the redemption window. The sale pays off the judgment at closing; you keep the rest of the equity.

- If you can’t reinstate, can’t redeem, can’t sell traditionally fast enough, and don’t have time: CASH SALE. We close in 7-14 days. The sale pays off the judgment, ends the foreclosure, and preserves whatever equity is left.

Frequently Asked Questions

What is reinstatement under Wisconsin foreclosure law?

Reinstatement under Wis. Stat. § 846.05 means bringing the mortgage loan current by paying all past-due amounts plus late fees, interest, attorney fees, and court costs. The loan continues on its original schedule. Reinstatement before judgment dismisses the foreclosure action; reinstatement after judgment but before sale stays the foreclosure but does not dismiss it.

What is redemption under Wisconsin foreclosure law?

Redemption under Wis. Stat. § 846.10 means paying off the entire foreclosure judgment (typically the full unpaid loan balance plus costs). After redemption, the loan ends and the foreclosure ends. The homeowner owns the property free and clear of that mortgage.

How long is the Wisconsin redemption period?

For owner-occupied 1-4 family residential property: 12 months from the date of judgment if the lender keeps the right to seek a deficiency judgment, or 6 months if the lender waives the deficiency. The election appears in the foreclosure complaint. During the redemption period the sheriff sale cannot occur.

Is it better to reinstate before or after judgment?

Before judgment is better. Pre-judgment reinstatement results in dismissal of the foreclosure action — a clean start. Post-judgment reinstatement only stays the action; if the borrower defaults again, the foreclosure proceeds without restarting. If reinstatement is possible, doing it before judgment preserves more protection.

Where Cash House Buyer WI Fits

Most of the homeowners I’ve worked with in this position have been somewhere in the redemption window — 3 to 9 months after judgment, sheriff sale scheduled or about to be scheduled, knowing they couldn’t pay off the loan but not knowing what other options existed. The cash sale path is straightforward: I make a written offer, we close, the title company pays off the judgment from closing proceeds, the rest of the equity is yours.

If you want to talk through which window you’re in and what the math looks like, call me directly at (414) 246-0032 or email Mike@cashhousebuyerwi.com. — Mike.